AP Microeconomics : Perfectly Competitive Markets

Study concepts, example questions & explanations for AP Microeconomics

All AP Microeconomics Resources

Example Questions

Example Question #1 : Perfectly Competitive Output Markets

If a monopolist's marginal cost curve shifts down, what is the expected effect on price and quantity of the monopolist's output?

Price decreases, Output decreases

Cannot determine either Price or Quantity.

Price decreases, Output increases

Price indeterminate, Quantity increases

Price decreases, Quantity indeterminate

Price decreases, Output increases

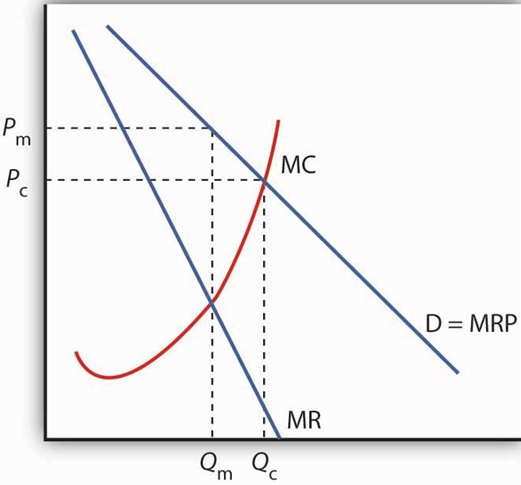

Although the monopolist will not end up producing at the socially optimal level, the effect of the change described is very similar to a shift in the supply curve in a perfectly competitive market.

Starting with the graph below as a baseline, you can see that if the marginal cost curve shifts down, the monopolist will produce at a point further along the marginal revenue curve, which would correspond to a greater output at a lower market price.

Example Question #1 : Perfectly Competitive Output Markets

A natural monopoly arises when which of the following characteristics of a perfectly competitive market are not met?

Well-defined property rights

Non-increasing returns to scale

Firms sell where marginal revenue equals marginal cost

Perfect information

Non-increasing returns to scale

A natural monopoly is defined by an industry where production is most efficient (i.e. lowest long-run average cost) when it is concentrated in a single firm. This implies increasing returns to scale, which is not characteristic of perfect competition. In other words, the natural monopolist will have a significant cost advantage over smaller competitors that try to enter the market.

Example Question #2 : Perfectly Competitive Output Markets

A natural monopoly differs from a traditional monopoly in what way?

Can set price by determining quantity of good to be sold

Lower average costs than same market with many firms

Positive economic profit in the long-run

Maximizes profits

High barriers to entry

Lower average costs than same market with many firms

A natural monopoly is very similar to and experiences the same inefficiencies as a traditional monopoly. The difference is that these inefficiencies cannot be corrected by increasing competition, as a single seller can produce more efficiently than many sellers in a market that is a natural monopoly.

Example Question #3 : Perfectly Competitive Output Markets

Assume that each of the following producers operates as a monopolist. Which one is most likely NOT a natural monopoly?

A producer of a patented drug

A railway network

A regional provider of electricity

A telecommunications provider

A producer of a patented drug

The electric company, railway, and telecoms operator are all examples of industries with very high fixed costs where the lowest average cost could only be achieved at a high level output, which discourages competition and is characteristic of natural monopoly.

The drug-maker operates as a monopoly due to the legal barrier (patent) that prevents entry into the market (for that specific drug). Therefore, it is NOT a natural monopoly.

Example Question #4 : Perfectly Competitive Output Markets

Assuming the markets for pencils and erasers are perfectly competitive, what is the expected effect on the market for pencils if there is a sudden shortage in the rubber needed to produce erasers?

Price increases, Quantity increases

Price increases, Quantity decreases

Price decreases, Quantity decreases

Cannot determine from information given.

Price decreases, Quantity increases

Price decreases, Quantity decreases

As pencils and erasers are used together they can be considered complementary goods. You can use a supply and demand graph for each market to track the following steps:

- The shortage in rubber shifts the supply curve in the eraser market inward

- As a result, the price of erasers increases

- Since pencils and erasers go together, a higher price for erasers means people demand fewer pencils at any given price.

- This results in an inward shift of the demand curve in the pencil market.

- As a result, both the price and quantity of pencils being sold goes down.

Example Question #11 : Competition

A price increase for Good A results in a decrease in the demand for Good B. Based on this information, Goods A and B are most likely...

Public goods

Inferior goods

Complementary goods

Substitute goods

Normal goods

Complementary goods

Complementary goods are defined by a negative cross elasticity of demand, which means simply that demand for one good increases when the price of another decreases (and vice versa). A price increase for Good A resulting in a decrease in demand for Good B fits this definition.

The goods are thus not substitutes. They could potentially be one of the other types of goods but you don't have enough information in the question to make that determination.

Example Question #42 : Ap Microeconomics

Which of the following pairs of goods are most likely NOT complementary goods?

Music books and artwork

Paper and pencils

Shoes and laces

Video games and game consoles

Music books and artwork

Some, or even many, people may love both music and art, but that does not suggest that music books and artwork are regularly purchased together. The other examples are goods that clearly work better together.

Example Question #41 : Ap Microeconomics

Which of the following would result in an increase in both the equilibrium price and quantity for a normal good?

Price of a substitute good decreases

Price of a complementary good decreases

A new subsidy for production of the good comes into effect

The government sets a price floor above the current market price

Price of a complementary good decreases

A decrease in the price of a complementary good would result in an outward shift in the demand curve, which is the only shift which would result in increased price and quantity of a given good.

A decrease in the price of substitute good would result in an inward shift of the demand curve. A subsidy for production would affect the supply curve. A price floor above the current equilibrium would necessarily affect the price, but not the quantity traded.

Example Question #42 : Ap Microeconomics

Coffee and tea can be considered substitutes for many consumers. Which of the following would result in an increased market price for coffee?

Production costs for tea falls

Production costs for tea increases

Production costs for coffee fall

Consumer income falls

Production costs for tea increases

An increase in production costs for tea results in an inward shift in the supply curve in the tea market. As a result, the market price of tea increases.

As tea becomes more expensive, consumers will prefer to consume more coffee at any given price. This is an outward shift in the demand curve that will result in a higher market price for coffee.

Example Question #43 : Ap Microeconomics

Which of the following examples of external costs/benefits might lead to a monopoly?

An individual who buys a particular software package increases the usefulness of that software for all other existing users

Bees raised for their honey help to pollinate surrounding crops

A person getting on the freeway at rush hour increases delay for all drivers behind them

Keeping your house and yard clean and maintained increases home values for those around you

An individual who buys a particular software package increases the usefulness of that software for all other existing users

The correct answer is an example of a "network externality." The software might be a video chat service or spreadsheet software and the more people who use it the more value it has for others who use the same format. If it reaches a so-called "tipping point" it may lead to one firm dominating the market.

All AP Microeconomics Resources